Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

- The Bank of Canada kept its policy rate at 0.25% (same level it has been throughout the pandemic), but is signalling that higher rates are coming soon.

- The Bank is ending quantitative easing (QE) and moving into the reinvestment phase, during which it will purchase Government of Canada bonds solely to replace maturing bonds. QE is a monetary policy tool in which a central bank attempts to stimulate growth in the economy by buying bonds or other financial assets in the open market to increase the money supply and encourage lending and investment.

- In Canada, robust economic growth has resumed, following a pause in the second quarter.

- The labour market conditions are also improving as indicated by the strong employment gains in recent months. However, labour shortages continue to persist in some sectors, as both employers and workers continue to search for skills and jobs respectively that are best suited to their individual needs.

- Housing activity is expected to remain upbeat, supported by high disposable incomes and low borrowing rates.

- The Bank expects CPI inflation to be elevated into next year and moderate back to around the 2% target by the backend of 2022.

Market Information •

November 5, 2021

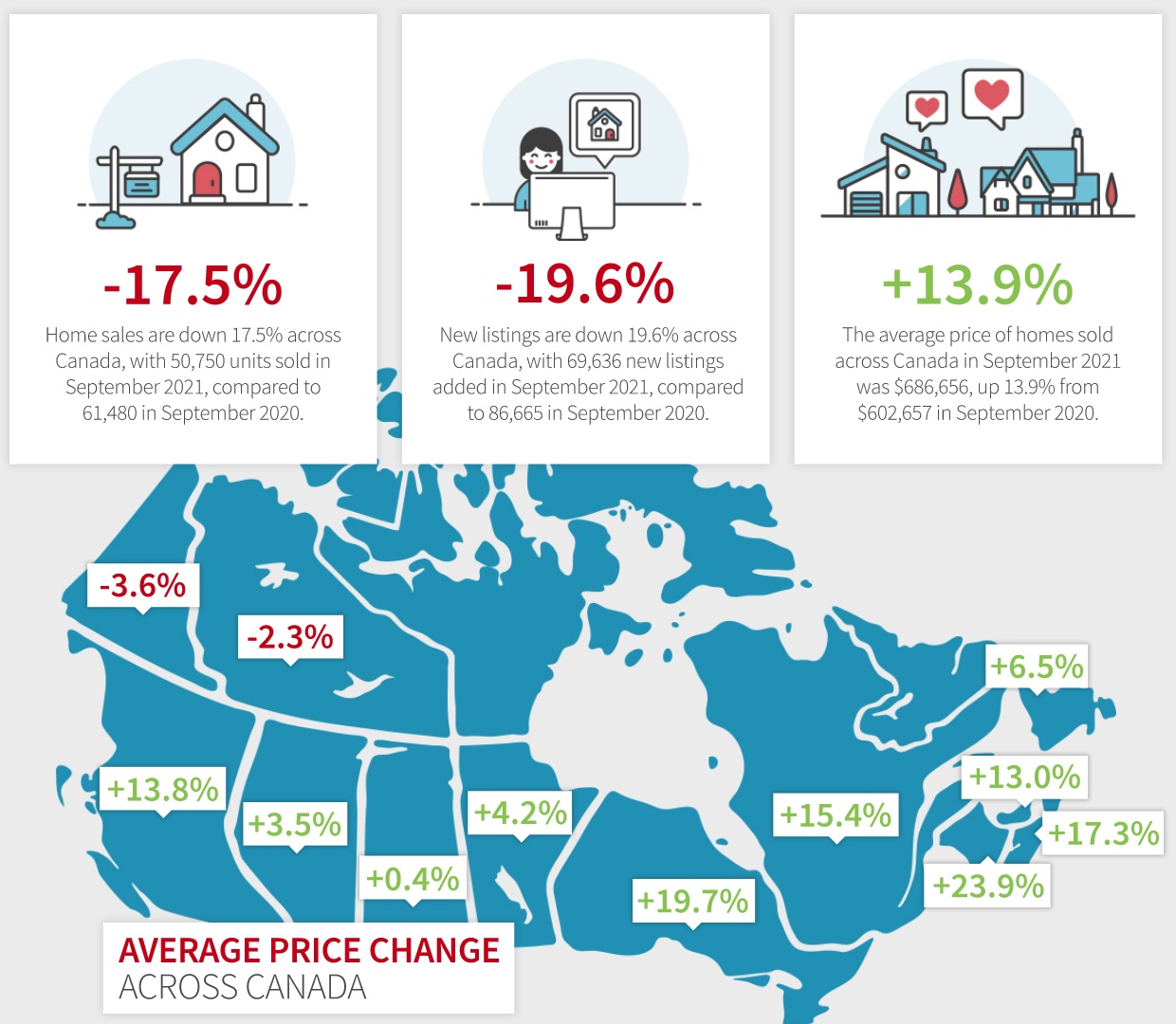

Market Highlights

Market Information •

November 4, 2021

UBC expanding presence in Surrey with $70M land acquisition

University of British Columbia’s expansion to Surrey is another indicator of the City’s rising prominence in the region. UBC Properties Trust has acquired a 135,000-square-foot property at the intersection of King George Boulevard and Fraser Highway. This project will definitely provide more opportunities to access post-secondary education and skills training in the fast-growing Fraser region.

Learn more about this news here: https://news.ubc.ca/

Seller's Information •

October 26, 2021

Home Seller Checklist: Before You List

Before listing your home, consider these factors to help you get the best price for your property and save you from all the hassle and stress.

1. Hire the right real estate professional who will look after your best interest. Selling a property  can be very stressful and time-consuming. Let an expert guide you through the process, help you negotiate the best price for your property, and ensure that everything is done efficiently. Choose a realtor that is knowledgeable about the market, professional, listens and communicates with you through-out the process.

can be very stressful and time-consuming. Let an expert guide you through the process, help you negotiate the best price for your property, and ensure that everything is done efficiently. Choose a realtor that is knowledgeable about the market, professional, listens and communicates with you through-out the process.

2. Review your financial plan with your financial advisor. It is always a good  practice to revisit your financial goals regularly and see where you are at in terms of home equity, progress of your investments, and overall financial health. If you want to buy another property using the proceeds of your sale, determine if you have enough equity on your home to use for down payment, if your current mortgage is portable, or if you will incur significant prepayment penalties as a result of paying off your current mortgage, and any other information that will help you plan your next steps.

practice to revisit your financial goals regularly and see where you are at in terms of home equity, progress of your investments, and overall financial health. If you want to buy another property using the proceeds of your sale, determine if you have enough equity on your home to use for down payment, if your current mortgage is portable, or if you will incur significant prepayment penalties as a result of paying off your current mortgage, and any other information that will help you plan your next steps.

3. Determine and prioritize the house repairs and improvements needed and create a budget for these expenses. Focus on the most important repairs and improvements to increase the  market appeal and resale value of your home. According to the Appraisal Institute of Canada, the renovations that generate the highest return on investment are—in this order—the kitchen, bathroom and interior and exterior painting, updating décor such as lighting and plumbing fixtures, countertops, curtains, cabinet hardware and flooring, and decluttering. For example, the kitchen represents 10% to 15% of a property’s value. If you want to renovate it, limit your expenses to that proportion of the home’s value. Kitchen renovations typically pay back about 75% to 100% of their cost, making them the most valuable home renovation investment. You can calculate the cost of your renovation either by determining the cost of your selected materials against the number of square feet being renovated or full cost method that takes into account the different professional trades needed for your renovations and the cost of the required materials.

market appeal and resale value of your home. According to the Appraisal Institute of Canada, the renovations that generate the highest return on investment are—in this order—the kitchen, bathroom and interior and exterior painting, updating décor such as lighting and plumbing fixtures, countertops, curtains, cabinet hardware and flooring, and decluttering. For example, the kitchen represents 10% to 15% of a property’s value. If you want to renovate it, limit your expenses to that proportion of the home’s value. Kitchen renovations typically pay back about 75% to 100% of their cost, making them the most valuable home renovation investment. You can calculate the cost of your renovation either by determining the cost of your selected materials against the number of square feet being renovated or full cost method that takes into account the different professional trades needed for your renovations and the cost of the required materials.

4. Check the Exterior/Curb Appeal. The first impressions are extremely important and the first  things that the buyers will see of your home are its exterior and “curb appeal”. According to a joint study by the University of Alabama and the University of Texas at Arlington, homes with high curb appeal tend to sell for an average of 7% more than similar houses with an uninviting exterior. So make sure that the lawn is freshly cut, the driveway is shoveled, and the walkway is cleaned.

things that the buyers will see of your home are its exterior and “curb appeal”. According to a joint study by the University of Alabama and the University of Texas at Arlington, homes with high curb appeal tend to sell for an average of 7% more than similar houses with an uninviting exterior. So make sure that the lawn is freshly cut, the driveway is shoveled, and the walkway is cleaned.

5. Depersonalize your space. Remove any distractions like personal family photos,  personal collections, or loud accent walls, so the buyers can visualize themselves and their family living in the property. Try to see it through the buyer’s eyes and create a blank slate for them to imagine themselves there.

personal collections, or loud accent walls, so the buyers can visualize themselves and their family living in the property. Try to see it through the buyer’s eyes and create a blank slate for them to imagine themselves there.

6. Get your home show ready. Declutter your home and take your excess stuff to storage off site or donate it. This will make your home more appealing to potential buyers and will  also make it easier to move out when your property sells. Refreshing the paint color of your walls to neutral tone is an easy way to breathe new life into your home. Also make sure your home smells good by taking the garbage out regularly and cleaning out pet areas.

also make it easier to move out when your property sells. Refreshing the paint color of your walls to neutral tone is an easy way to breathe new life into your home. Also make sure your home smells good by taking the garbage out regularly and cleaning out pet areas.

Thinking of selling your home? Let’s discuss how we can quickly start working on the next steps!

Buyer's Information •

October 20, 2021

Homebuyer Guide: When do I start planning and preparing if I want to buy a property?

I recommend to start early. As soon as you start working and able to contribute  to your Registered Retirement Savings Plans (RRSPs), you can set aside a portion of your disposable income monthly to save for the down payment.

to your Registered Retirement Savings Plans (RRSPs), you can set aside a portion of your disposable income monthly to save for the down payment.

Did you know that you can use your RRSP for down payment if you are a first-time homebuyer? This is called the Home Buyers’ Plan (HBP) and it is a program that allows you to withdraw funds of up to $35,000 tax-free from your RRSPs to buy or build a qualifying home for yourself or for a related person with a disability. You just pay back the withdrawn funds within a 15-year period.

Once you have decided that you want to buy your dream home, allow yourself abundant time to plan,  research and talk to your trusted realtor and financial institution if you are applying for a mortgage, I would say 6 months to a year. The mortgage application process may take a few days to weeks depending on the complexity of your application. You have to factor in the financial institution’s processing time, the appraisal, inspection, notary or lawyer processing time among other things.

research and talk to your trusted realtor and financial institution if you are applying for a mortgage, I would say 6 months to a year. The mortgage application process may take a few days to weeks depending on the complexity of your application. You have to factor in the financial institution’s processing time, the appraisal, inspection, notary or lawyer processing time among other things.

My experience as a financial planner and lender sets me apart from the rest so contact me today to discuss and develop a plan to make that dream of owning a home a reality!